The Bank Never Showed Up. So YouLend Did.

- F.I. Editorial Team

- Mar 7

- 7 min read

YouLend just secured $225 million to lend money to small businesses, but the remarkable thing isn't the size. It's the mechanism. The loan never comes from a bank. The merchant never fills out a form. The money arrives through the software they were already using.

Picture a small business owner in Atlanta, let's call her Maria. She runs a clothing brand on Shopify. Business is good; she wants to buy inventory ahead of the summer season but needs $40,000 in working capital. She goes to her bank. The bank asks for two years of tax returns, a personal guarantee, three months of bank statements, and tells her she'll hear back in four to six weeks. She doesn't have four to six weeks. The inventory needs to be ordered now.

Maria logs back into Shopify. There's a banner she's never paid attention to. It says she's been pre-approved for $47,500 based on her sales history. She clicks it, confirms the amount, and the money hits her bank account the same day. Repayment comes automatically, a small percentage of each sale, so she never has to think about it again.

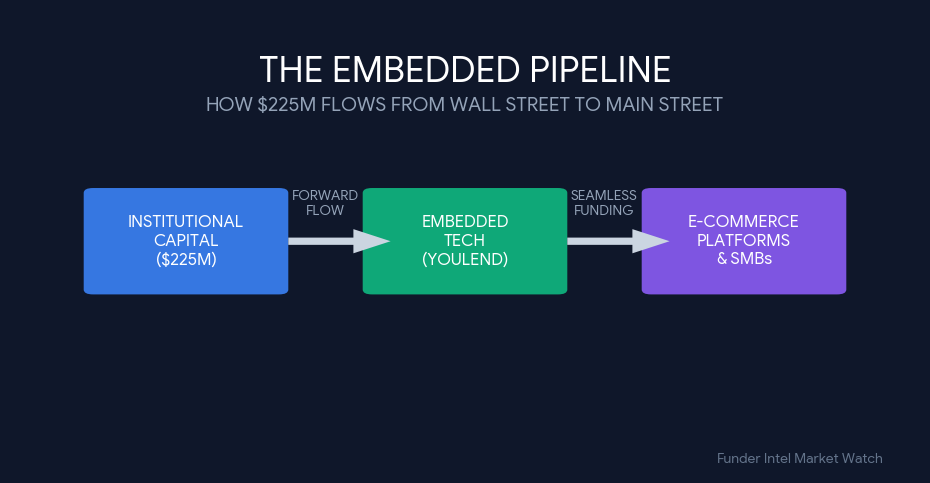

She doesn't know it, but the company that actually underwrote that loan wasn't Shopify. It was YouLend. And the capital YouLend just used to fund her came, in part, from a $225 million forward-flow facility it announced this week with Värde Partners, a global alternative investment firm.

That's not just a fintech deal. That's the story of how small business lending works now.

What YouLend Actually Does

Founded in 2016 in London, YouLend is what the industry calls an embedded financing platform, and to be more specific, embedded lending. It doesn't have branches. It doesn't advertise to small businesses directly. Its entire distribution strategy is to disappear inside the software that small businesses already use, e-commerce platforms, payment processors, accounting tools, and surface capital offers at precisely the moment a merchant needs money.

The company's technology integrates via API with host platforms. The platform shares transaction data. YouLend's model assesses creditworthiness not through traditional credit scores but through actual business performance, revenue trends, transaction frequency, platform tenure, return rates. The result is a 90% approval rate and funding in as little as 24 to 48 hours, compared to the four-to-six-week wait that Maria's bank quoted her.

The product is revenue-based financing: merchants repay as a percentage of daily sales, which means repayment flexes with the business. A slow week means smaller payments. A strong week means faster payoff. There's no fixed monthly bill, no penalty for early repayment, no collateral requirement. For a small business whose revenue is seasonal or unpredictable, this structure is genuinely different from anything a traditional lender offers.

To date, YouLend has provided funding to more than 370,000 businesses globally. Its partners include Shopify, eBay, Amazon, and Dojo. That number, 370,000 businesses, is worth sitting with for a moment. That's 370,000 instances of capital reaching a business that, in many cases, would have been turned away by a traditional lender.

The Värde Deal: What $225 Million in Receivables Actually Means

The structure of this transaction deserves more attention than the headline number. This is not a fundraise. YouLend isn't selling equity. What Värde Partners has agreed to do is purchase up to $225 million in receivables, the future repayment streams from loans YouLend has already originated or will originate. It's a forward-flow agreement, which means Värde commits in advance to buying those receivables as they're created, giving YouLend a predictable, scalable pool of capital to deploy.

For YouLend, this is elegant. It gets committed U.S. capital without tying up its own balance sheet. As it originates new loans, Värde purchases them. The risk of those loans sits on Värde's books. YouLend earns fees for origination, servicing, and platform management. It can grow its lending volume without needing to raise equity rounds every time it wants to expand.

For Värde, this is asset-backed private credit, a category that institutional investors have been racing toward as traditional fixed income yields have compressed. The receivables are backed by real small business repayments, diversified across hundreds or thousands of merchants. The default risk is pooled, underwritten by YouLend's platform data, and structured to give Värde predictable cash flows.

"Värde's deep experience in U.S. asset-backed credit and specialty finance makes them a strong partner as we continue to invest in our U.S. capabilities and meet growing merchant demand in this core market."— Gaurav Maheshwari, Head of Capital Markets, YouLend

This is not YouLend's first major capital markets move in the U.S. In October 2024, the company secured a separate $1 billion facility from Castlelake, another alternative investment firm, to fund U.S. SMB originations over a three-year window. The Värde deal layered on top of Castlelake signals something important: YouLend is deliberately diversifying its institutional capital base. Multiple forward-flow partners reduce concentration risk and give the business more flexibility to grow without being dependent on a single counterparty's appetite or credit terms.

The Quiet War Between Banks and Platforms

To understand why YouLend's model is working so well right now, you need to understand what happened to small business lending over the past decade, and what happened to it in 2025 specifically.

Banks have always been poor at lending to small businesses. Not because they don't want to, but because the economics are brutal. Underwriting a $50,000 loan costs roughly the same in compliance, documentation, and credit analysis time as underwriting a $5 million loan. The margin on the small loan is a fraction. So banks naturally gravitated toward larger commercial clients, leaving a persistent gap in the market for businesses that needed $10,000 to $500,000 quickly.

That gap has historically been filled by credit cards, personal loans, and predatory short-term lenders who charge rates that would make a loan shark blush. The embedded lending model doesn't just improve on those options; it replaces the entire paradigm. When the platform that processes your payments is also the one extending you credit based on those payments, the underwriting is fundamentally different. No forms. No human review process. No four-week wait.

"Embedded banking lets accounting platforms and marketplaces own the full financial workflow, relegating banks to back-end infrastructure providers."— Riccardo Colnaghi, Industry Analyst — 2025

The data from 2025 shows this shift is now measurable at scale. Shopify's gross loans receivable reached $1.6 billion at year-end 2025, up 43% from $1.1 billion a year earlier. The company purchased $4.2 billion in merchant cash advances and loans during 2025, compared to $3 billion in 2024. Block reported that Square Loans were the primary driver of its Financial Solutions growth in Q4. PayPal's working capital products continue to expand. JPMorgan, meanwhile, reported muted growth in consumer lending margin, in part because fintech partners are cutting into origination fees that banks used to own.

The moat that banks spent decades building, transaction data and customer relationships, has shifted. The platforms that process payments now own the data. And the companies that power those platforms' lending products, like YouLend, are the new infrastructure layer for small business credit in America.

Why the U.S. Matters So Much

YouLend is a London-born company that has operated primarily in the UK and the European Union. Its U.S. expansion is deliberate, well-resourced, and now better capitalized than ever, but it is still, in relative terms, in its early days.

The U.S. SMB market is simply enormous. Small and medium-sized businesses account for between 43.5% and 50.7% of U.S. GDP. They represent 62.7% of all net new job creation historically. The National Small Business Association has consistently found that access to capital is one of the top constraints on small business growth, with roughly one in four small businesses reporting they were unable to get the financing they needed in the past year.

That unmet demand is precisely the market YouLend is targeting. The Castlelake facility funded originations. The Värde facility adds $225 million more, structured to grow as YouLend's U.S. platform scales. The company recently expanded into a larger Atlanta headquarters to support its growing American team, a physical signal of the organizational investment behind the capital one.

The embedded finance market in the U.S. is projected to exceed $7 trillion in transaction value by 2026, according to multiple industry reports. Embedded lending alone, the slice YouLend occupies, is forecast to reach $80 to $90 billion in outstanding balances. YouLend is not the only company chasing that number. But it has platform partnerships, institutional capital relationships, and a decade of proprietary lending data that make it one of the most credibly positioned players to capture a meaningful share of it.

The Bigger Picture for Alternative Lenders

For anyone operating in the alternative lending space, merchant cash advances AKA revenue-based financing, and business term loans, the YouLend story is both an opportunity signal and a competitive warning.

The opportunity: embedded lending infrastructure is still early, and the distribution advantage it creates is enormous. A lender that integrates natively into a platform where merchants already spend hours every day has a customer acquisition cost that approaches zero. The merchant doesn't shop for a loan. The loan finds them. That is a structural advantage that standalone alternative lenders cannot easily replicate.

The warning: the same structural advantage that benefits YouLend is also what allows Shopify, Square, and PayPal to build their own lending products in-house. As those giants grow their loan books, Shopify at $1.6 billion and climbing, the addressable market for independent embedded lenders gets both larger and more competitive simultaneously.

What YouLend has done well is position itself as an infrastructure for the mid-tier and smaller platforms that can't build their own lending products internally. It's the lender you call when you're eBay, Etsy, or Dojo, large enough to want an embedded capital offering for your merchants, not large enough to build and fund it yourself. That middle market is deep, growing, and in need of exactly what YouLend offers.