AI in Equipment Finance: Inside Lendscape's MCP Server

- F.I. Editorial Team

- 3 hours ago

- 4 min read

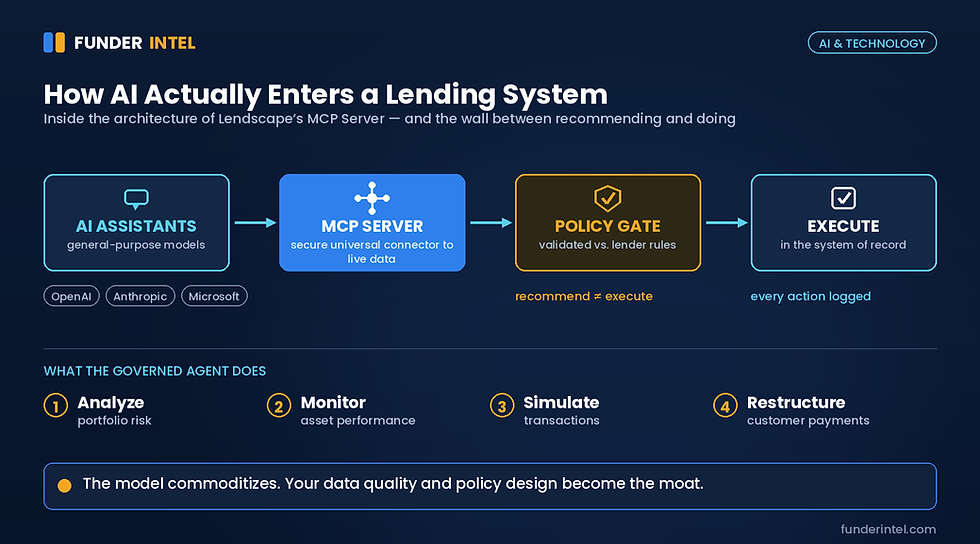

A new “MCP Server” lets AI assistants from OpenAI, Anthropic, and Microsoft act inside a lender’s live systems, not just talk about them. The real innovation isn’t the AI. It’s the wall between recommending and doing.

The headlines about AI in lending have mostly been about the front door: faster underwriting, instant approvals, the origination speed race. The more consequential shift may be happening at the back door, in the unglamorous machinery of servicing, collections, and portfolio management. That’s where Lendscape just planted a flag.

Lendscape, the roughly 50-year-old London-based software provider whose platforms underpin secured commercial lending for more than 120 banks and finance companies and some $200 billion in annual lending, has launched what it calls a Model Context Protocol (MCP) Server. As reported by Equipment Finance News, the tool connects a lender’s live Lendscape environment to AI assistants from OpenAI, Anthropic, and Microsoft, letting them access operational data, analyze portfolios, simulate transactions, and execute approved actions inside the lender’s own guardrails.

First, What “MCP” Actually Means

If “Model Context Protocol” means nothing to you, here’s the short version. MCP is an open standard, originally introduced by Anthropic and since adopted across the major AI providers, for connecting AI models to outside software and data. Think of it as a universal adapter, a USB-C port for artificial intelligence. Instead of every lender building a bespoke, brittle integration for each AI tool, MCP gives any compliant AI a standard, secure way to plug into the system of record and actually use it. It’s the difference between an assistant who can describe how to restructure a payment and one who can pull the live account, model the restructure, and, if the rules allow, carry it out.

The Real Innovation Is the Wall

That last clause is the whole story. The genuinely interesting part of Lendscape’s launch isn’t that AI can touch a loan-servicing system; it’s the architecture around what happens next. The MCP Server separates recommendation from execution: an AI can propose an action, but nothing happens until it is validated against the lender’s own policies, and every step is recorded in an auditable trail. In a regulated business, that wall isn’t a limitation; it’s the feature that makes AI usable at all. It turns a clever conversational tool into something a compliance officer can actually sign off on.

Why the Back Office Is the Smart Target

Why does this matter more than another origination-AI story? Because the back office is where the work actually piles up and where the return is cleanest. Servicing thousands of small-ticket contracts, chasing payments, monitoring asset performance, restructuring the accounts that wobble, this is labor-intensive, rules-bound, and endlessly repetitive, which is precisely what supervised AI agents are good at. Origination AI competes on speed; back-office AI competes on cost-to-serve, and it does so on tasks where a mistake is recoverable and logged rather than a blown credit decision baked into a five-year contract.

The Shift Underneath

Step back, and the strategic picture sharpens. When any AI model can plug into your system through a common protocol, the model itself starts to commoditize. The differentiator moves to two things you actually control: the quality of your data and the clarity of your policies. An agent wired into a clean, well-governed system with crisp rules becomes a tireless junior employee. The same agent wired into messy data and vague guardrails becomes a fast way to make mistakes at scale. The competitive edge in AI-era lending will belong to the operators who did the boring work of data hygiene and policy design first.

What It Means for the Channel

For equipment lenders, funders, and the brokers who depend on them, a few things follow. Cost-to-serve is about to become a real battleground; shops still running servicing and collections on manual labor will feel the margin pressure as competitors automate. Smaller players aren’t necessarily locked out; the entire point of a standard like MCP is that capability arrives through software rather than a giant in-house data-science team, but they’ll need clean systems to take advantage of it. And the vendors are plainly racing: rivals are re-platforming as “AI-native,” which means lenders will soon be choosing technology partners as much on their AI plumbing as on their core features.

The Case for Caution

A few caveats keep this honest. Agentic AI in collections and servicing brushes up against real consumer- and commercial-protection sensitivities; “execute approved actions” is only as safe as the policies doing the approving, and regulators will expect those guardrails and audit trails to hold up under scrutiny. Automating a process built on bad data simply industrializes the errors. And there’s a quieter strategic question in standardizing on any single protocol or vendor stack, convenient today, worth thinking through for lock-in tomorrow. None of this is a reason to wait on the sidelines. It’s a reason to step in with eyes open.

The Bottom Line on Lendscape

The origination stories get the attention because speed is visible. But the Lendscape launch points at something more durable: AI graduating from a tool you talk to into a supervised actor wired into the core of the business, with a hard wall between what it suggests and what it’s allowed to do. The model was never going to be the hard part. The guardrails are. The lenders who treat policy design and data quality as competitive assets, not compliance chores, are the ones who will get the most out of the agents now showing up for work.

Comments